Messari: Trading US Stocks on Perp DEX, the Next New Frontier

Original Article Title: Equity Perps: Tall Orders and Slow Beginnings

Original Article Author: Sam, Messari Research

Original Article Translation: Deep Tide TechFlow

Key Insights:

Equity perpetual contracts still belong to a high-potential but unproven area, with limited appeal in the on-chain market mainly due to misaligned audience, weak demand, and more popular alternatives (such as 0DTE options).

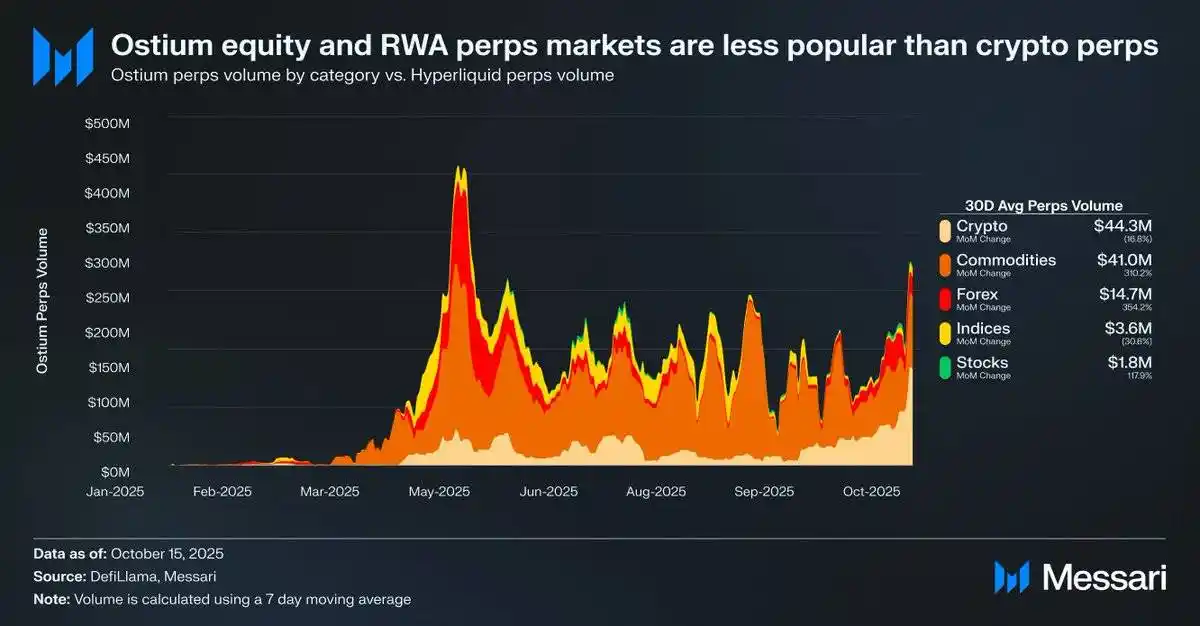

For example, the daily average trading volume of equity perpetual contracts on the Ostium platform is only $1.8 million, while cryptocurrency perpetual contracts reach as high as $44.3 million, demonstrating a weak market demand.

This may imply that due to infrastructure and regulatory constraints, market demand has not been fully unleashed. Hyperliquid's recent HIP-3 upgrade has provided the best opportunity for equity perpetual contracts, but the adoption process is expected to be gradual.

Source: Messari (@0xCryptoSam)

Equity perpetual contracts are considered the inevitable next blue ocean in the on-chain market, but current data suggests that this area is still challenging to break through in the short term. Ostium, as a decentralized exchange focusing on real-world assets (RWAs), has a daily average trading volume of equity perpetual contracts of only $1.8 million, while cryptocurrency perpetual contracts reach $44.3 million, reflecting weak demand.

This adoption gap is mainly due to misaligned audience. On-chain traders have little interest in stocks, while off-chain platforms (such as Robinhood) allow traders to easily trade stocks and options but not perpetual contracts. International investors may be a potential target audience as they cannot directly access the US stock market. However, these investors may prefer to hold stocks directly to gain shareholder rights while avoiding funding costs and settlement risks.

Compared to tokens, stocks have fewer interoperability challenges, benefiting from the convenience of synthetic wrapping. For the average investor, almost every stock in the global market has already been abstracted through the search bar's individual stock code. Therefore, even though perpetual contracts add permissionless and censorship-resistant features to stocks, ordinary stock investors are either unaware of this or simply not interested.

Source: fow

The most likely users of stock perpetual contracts are retail options traders (who drive 50%-60% of 0DTE trades on the Robinhood platform). However, traditional exchanges relying on banking services will only adopt stock perpetual contracts when the law is clear. The U.S. Commodity Futures Trading Commission (CFTC) has approved perpetual contract trading for BTC and ETH, but these two have been deemed non-securities. While perpetual contracts are more intuitive than options, the popularization of stock perpetual contracts may be slower than expected due to the close link between retail adoption paths and legal clarity.

Source: @Kaleb0x

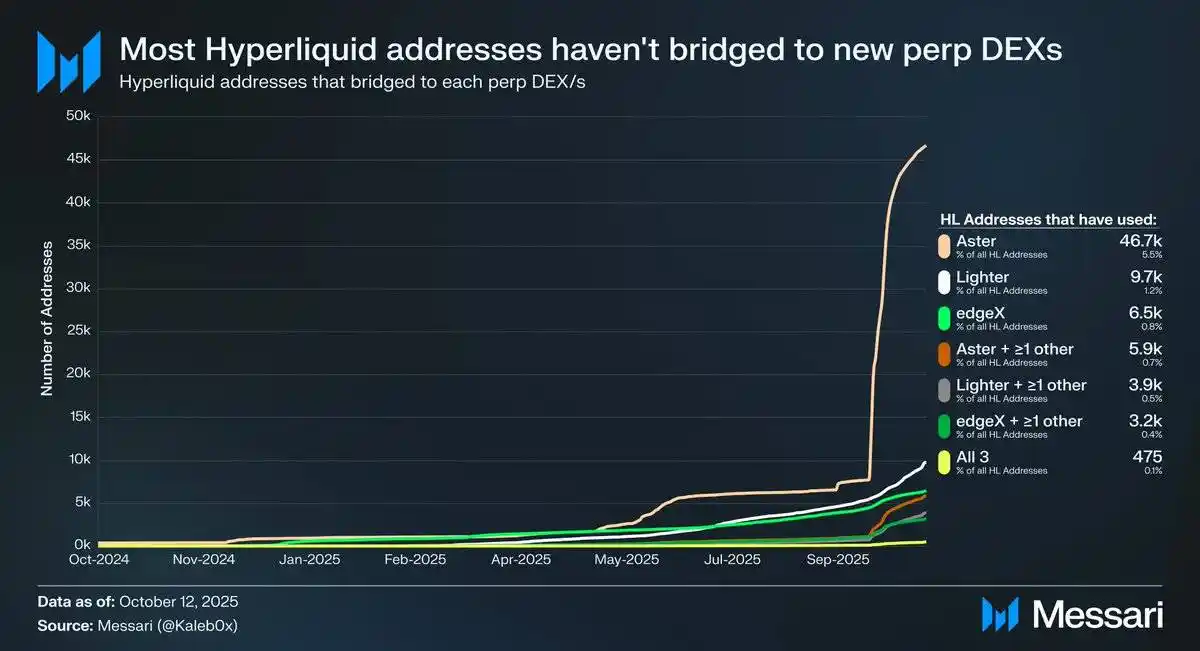

Let's discuss the potential development direction of stock perpetual contracts under the background of the HIP-3 upgrade on Hyperliquid. HIP-3 introduces a permissionless perpetual contract market, and data shows that less than 10% of Hyperliquid addresses have bridged to Aster, Lighter, and edgeX, with even fewer users opting for multiple perpetual contract decentralized exchange (DEX) platforms. This indicates that funds on Hyperliquid are sticky and of higher quality. Based on this data, the future of stock perpetual contracts can be predicted from two perspectives:

Hyperliquid users are loyal to the platform and, regardless of asset listings or features, they are more likely to choose Hyperliquid over other perpetual contract DEXs.

Hyperliquid users are satisfied with the current perpetual contract market products.

I believe both of these viewpoints make sense. Considering that Hyperliquid users have not massively shifted funds in the face of incentives, they may be loyal to Hyperliquid. However, as most of the trading volume and open interest on Hyperliquid are concentrated in mainstream assets, similar to other perpetual contract DEXs, it is currently difficult to determine whether Hyperliquid users care about market diversity and whether stock perpetual contracts are attractive to regular users (more importantly, to the whales holding 70% of Hyperliquid's open interest).

In addition, these traders may also have accounts on both traditional trading platforms and brokerage platforms, further limiting the potential market size of stock perpetual contracts on Hyperliquid.

It is worth noting that stock perpetual contracts may not bring new open interest or trading volume to Hyperliquid but may instead divert existing trading volume.

Although Ostium (with an annual average perpetual contract trading volume of $220 billion) and stock tokenization tools (such as xStocks, with a spot trading volume of $2.79 billion) have not yet experienced explosive growth, this may reflect infrastructure limitations rather than a lack of underlying demand. This pattern mirrors the early growth trajectory of perpetual contracts. GMX demonstrated the demand for on-chain perpetual contract markets, but the infrastructure at the time could not support sustained trading volume. Hyperliquid overcame this bottleneck, unleashing latent demand. By the same logic, after stock perpetual contracts receive the necessary performance and liquidity enhancements under HIP-3, they may find their first scalable product-market fit on Hyperliquid. While current data cannot confirm this outcome, this precedent is worth noting.

Compared to 0DTE options, the long-term potential of stock perpetual contracts remains evident. Projects like Trade[XYZ] can leverage regulatory arbitrage to build an early user base before entering the market on traditional exchanges. However, the real challenge lies in attracting off-chain retail traders, which has always been difficult for crypto applications.

You may also like

Morning Report | CoinEx becomes a key hub for Iran to evade sanctions, involving over $3.8 billion in funds; Kalshi seeks a new round of financing, with a valuation potentially rising to $40 billion

From the white-haired stock god to the billionaire fund mogul, the smart people shorting Nvidia are all getting rich using the same framework

Why do cryptocurrency projects always like to change their names?

Global Launch: As predictions become the most scarce asset in the AI era, Manadia is defining the next generation of the value internet

Who is footing the bill for the $64 billion accounting frenzy?

I never expected that the first application of AI x Crypto would be in security auditing

What is your view on Binance's competitive advantages?

ETH has entered a non-consensus phase, and the turning point is approaching!

The shift in the cloud of the air: from despising stablecoins a year ago to the high-profile entry of capital today

The survival dilemma of small and medium exchanges behind the withdrawal anomalies exposed by AscendEX

Why Is Bitcoin Falling Below $60K? 5 Key Market Drivers Explained

Bitcoin has dropped sharply amid ETF outflows, Strategy stock weakness, AI stock rallies, and changing Fed expectations. Explore the key forces driving BTC’s latest correction and what traders should watch next.

Bitcoin vs. Gold in 2026: Which Asset Performs Better in Different Markets?

Morning News | The draft amendment to the People's Bank of China Law aims to clarify the legal status of digital renminbi; South Korea will transfer about 40 unregistered virtual asset service providers to law enforcement agencies

The cryptocurrency industry has entered the "Show Me" era: merely relying on vision is no longer enough

Interpreting the Ethereum Foundation's new structure: Reaffirming self-sovereignty amid institutional trends

Former SpaceX engineer reconstructs the financial execution system using first principles

Standard Chartered Bank sings a 50x rhapsody again, aiming for AAVE to reach 3500 USD